Have you ever looked at the monthly payments for a brand-new car and felt a sudden wave of sticker shock? You are not alone. As new vehicle prices and interest rates continue to climb, many smart shoppers start looking for creative ways to save money while still driving a reliable vehicle. You might find yourself asking one very specific question: can you lease a used car?

Most drivers assume that leasing only applies to shiny, brand-new models sitting directly on the dealership showroom floor. However, the automotive market offers much more flexibility than you might realize. You absolutely can lease a used car. While the process looks and operates a bit differently than a traditional new car lease, it opens the door to significant savings and comfortable monthly payments.

In this comprehensive guide, we will explore exactly how used car leasing works. We will help you understand your used car lease options, explain the distinct benefits of leasing a certified pre owned car, and break down the costs involved. Whether you want to drive a premium luxury vehicle on a strict budget or you simply need a dependable daily commuter, this article will show you if you can lease a second hand car that perfectly fits your lifestyle.

Let us dive into the details and find out if a used car lease makes the most financial sense for your next vehicle.

Can You Lease a Used Car

Yes, you can lease a used car. However, you will not see flashy commercials advertising this option on television, and you cannot walk into just any local independent car lot and ask for a used lease. Dealerships keep these options relatively quiet, and they only offer them under very specific conditions.

When you lease a brand-new car, the automaker’s dedicated financial branch usually backs the deal. The manufacturer wants to move fresh inventory off the lot to make room for next year’s models. Used cars represent a totally different challenge for financial institutions. Every single used car has a unique history, a different mileage reading, and varying levels of wear and tear. This uniqueness makes it incredibly difficult for banks to predict exactly how much the car will be worth at the end of a lease term.

Because of this financial unpredictability, you generally cannot lease a random eight-year-old vehicle from an independent used car lot. Instead, you will need to look at specialized used car leasing programs. These official programs mostly exist at franchised dealerships—dealerships directly affiliated with a major global automaker like Toyota, Lexus, Ford, or BMW.

Some specialized independent leasing companies also offer used car leases. They purchase vehicles from wholesale auctions or take returns from new car leases and lease them back out to budget-conscious customers. However, the safest, most reliable, and most common route involves visiting a franchised dealer and asking the finance manager about their specific used lease programs.

How Used Car Leasing Works

To fully understand how you can lease a second hand car, you must first understand the basic mechanics of auto leasing. When you lease a vehicle, you do not pay for the entire purchase price of the car. Instead, you only pay for the value the car loses while you drive it. The automotive industry calls this loss in value “depreciation.”

Here is exactly how the dealership and the bank calculate your used car lease:

First, the dealer sets the current starting price of the vehicle. The leasing industry calls this the capitalized cost. Next, the leasing company estimates the car’s future value. This is the residual value—the exact amount of money the leasing company believes the car will be worth at the end of your lease term. Finally, the leasing company subtracts the residual value from the capitalized cost. The difference between these two numbers equals your total depreciation.

You pay this depreciation amount spread out over your lease term, which usually lasts between 24 and 36 months. Alongside the depreciation, you also pay a finance fee, which the dealer calls the money factor, plus local sales taxes.

Because used cars have already gone through their steepest and most aggressive depreciation phase during their first few years on the road, the financial gap between the capitalized cost and the residual value shrinks significantly. A smaller depreciation amount directly results in a drastically lower monthly payment for you.

A Practical Example of a Used Car Lease

Let us look at a practical, real-world example to make this math crystal clear. Imagine you want to lease a three-year-old midsize sedan.

- The dealer prices the used car today at $20,000 (Capitalized Cost).

- The leasing bank estimates that after your three-year lease, the car will have a value of $14,000 (Residual Value).

- The car will depreciate by $6,000 during your time driving it.

- You only pay that $6,000 (plus your taxes and money factor fees) divided evenly over 36 months.

This simple calculation creates a much smaller monthly payment compared to leasing a brand-new $35,000 version of the exact same car, which might drop $15,000 in value over those same three years.

Leasing a Certified Pre Owned Car

If you want to lease a used vehicle, your absolute best and safest option involves leasing a certified pre owned car. Most major automakers that allow used car leasing restrict their financing programs exclusively to their Certified Pre-Owned (CPO) inventory.

What makes a CPO car so much different from a standard used car? Dealerships only select the highest-quality, best-condition vehicles for their CPO programs. Usually, these cars recently returned to the dealership after a previous two or three-year lease ended. The dealer puts the vehicle through a rigorous, multi-point physical inspection. The factory-trained mechanics check everything from the engine performance and brake pad thickness to the interior upholstery and exterior paint condition. If a specific part does not meet the strict manufacturer standards, the dealer immediately repairs or replaces it.

Because the original manufacturer guarantees the quality and reliability of these specific vehicles, the financing bank feels confident enough to accurately predict the residual value and offer you a lease.

Automakers usually place strict operational limits on which CPO cars qualify for a lease. Typically, the vehicle must meet the following criteria:

- The car must be fewer than four model years old.

- The car must have fewer than 48,000 miles on the odometer.

- The car must pass the official CPO inspection and reconditioning process.

Luxury brands like Acura, Audi, BMW, Lexus, Mercedes-Benz, and Porsche frequently offer the best used car lease options. Luxury cars lose their value incredibly fast in the first few years, which makes a CPO lease an excellent way to drive a premium, high-end vehicle for a mere fraction of the new-car price. Mainstream brands like Honda, Hyundai, and Toyota also offer these programs, though you might need to call several local dealerships to find one that actively promotes them to customers.

Important Note for Readers: Not every single dealership participates in CPO leasing, even if the parent manufacturer allows it. Dealer policies vary widely from city to city. You should always call the dealership’s finance department ahead of time to confirm they offer formal used car leasing programs.

Pros and Cons of Leasing a Used Car

Every single financial decision you make comes with natural trade-offs. Before you sign any binding dealership paperwork, you need to carefully weigh the benefits and drawbacks of a used car lease.

Advantages of leasing a used car

- Lower Monthly Payments: This remains the absolute biggest draw for consumers. Because the car has already survived its steepest depreciation curve, you finance a much smaller amount of money. This keeps more cash in your monthly budget for other expenses.

- Slower Depreciation: New cars lose up to 20 percent of their value the minute you drive them off the lot. A used car loses value at a much slower, steadier pace.

- Cheaper Auto Insurance: Auto insurance companies base your monthly premiums on the total replacement value of your vehicle. Since a used car costs less to replace than a new one, your insurance provider will likely charge you significantly less for comprehensive and collision coverage.

- Affordable Buyout Option: When your lease ends, the contract gives you the option to buy the car. Because the residual value of a used car is much lower than a new car, purchasing the vehicle at the end of the term becomes a very affordable and realistic financial option.

- Access to Higher Trim Levels: If a brand-new luxury car falls outside your budget, leasing a three-year-old version of the same car allows you to enjoy premium features, leather seats, and advanced technology for the exact same price as a standard new commuter car.

Disadvantages of leasing a used car

- Higher Maintenance Risks: Brand-new cars rarely break down, and when they do, a comprehensive bumper-to-bumper factory warranty covers almost everything. Used cars naturally have more wear and tear. While CPO vehicles include warranties, these warranties might not cover every single mechanical component, or they might expire before your lease ends. You could end up paying out of pocket for repairs on a car you do not even own.

- Higher Interest Rates: Banks and lenders view used cars as slightly riskier investments. To protect themselves, leasing companies often charge a higher money factor (the leasing version of an interest rate) on used cars compared to heavily subsidized new cars.

- Limited Availability: You cannot simply point to any attractive car on the lot and ask to lease it. Finding the exact make, model, and color you want in the authorized CPO lease inventory requires patience and extensive searching.

- Older Technology: When you lease a vehicle that is already three or four years old, you naturally miss out on the absolute newest safety features, infotainment software updates, and engine fuel efficiency improvements found in the current model year.

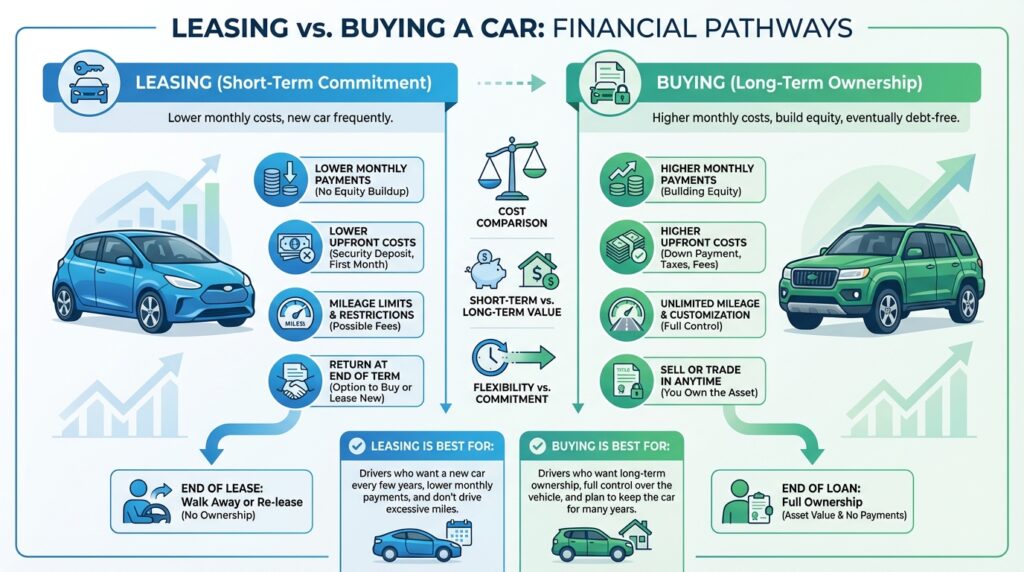

Used Car Lease vs New Car Lease

Choosing between a used car lease and a new car lease requires a careful look at your personal priorities. Do you value the absolute lowest possible monthly payment, or do you prioritize the ultimate peace of mind that comes with a brand-new vehicle?

To help you understand the core differences clearly, we have created a direct comparison table below.

| Feature | Used Car Lease | New Car Lease |

|---|---|---|

| Monthly Payment | Generally lower due to slower depreciation. | Generally higher due to rapid initial depreciation. |

| Vehicle Condition | A few years old, minor wear and tear, thousands of miles driven. | Flawless condition, zero wear, almost zero miles on the odometer. |

| Warranty Coverage | CPO warranty included, but might expire before the lease ends. | Full factory bumper-to-bumper warranty covers the entire lease term. |

| Choice and Availability | Limited to what the dealer currently has in the CPO inventory. | Unlimited choices. You can even custom order the car from the factory. |

| Insurance Costs | Lower premiums because the car holds a lower overall value. | Higher premiums due to the high replacement cost of a new vehicle. |

When you choose a new car lease, you pay a distinct premium for the famous “new car smell” and the pristine condition of the vehicle. The dealership hands you a car backed by a massive factory warranty. You also get the distinct privilege of picking the exact paint color, interior trim, and technology packages you want directly from the manufacturer.

When you look at used car lease options, you trade some of that pristine perfection for excellent financial flexibility. You willingly accept a car with a few thousand miles on it, and you must choose from whatever the dealer currently holds in stock. However, you benefit from a drastically reduced monthly payment, making it much easier to afford a nicer, higher-class vehicle than you could possibly buy brand new.

Requirements for Leasing a Used Car

Dealerships and auto financing companies set strict rules for anyone wanting to lease a vehicle. Because they hand over the keys to an expensive, depreciating asset, they need to ensure you will consistently make your payments on time and return the car in good working condition.

If you plan to walk into a dealer and ask, “can you lease a second hand car for me?”, you need to prepare the following items beforehand:

- A Strong Credit Score: Leasing generally requires a much better credit score than traditional auto financing. Most banks want to see a credit score of at least 670 to approve a used car lease. If you want the best money factor (the lowest interest rate), you should aim for a score above 720. If you have a lower credit score, you might still secure a lease if you bring a co-signer. A co-signer with excellent credit legally promises to make the payments if you fall behind.

- Proof of Stable Income: The dealership will ask for your recent pay stubs or bank statements. The finance manager calculates your debt-to-income ratio to make absolutely sure you can comfortably afford the monthly lease payment alongside your rent, mortgage, and other daily bills.

- Full Coverage Auto Insurance: You cannot lease a car with just basic liability insurance. The leasing company technically owns the vehicle, so they require you to carry comprehensive and collision coverage to protect their large investment in case of a severe accident.

- A Down Payment (Sometimes): While many dealers aggressively advertise zero-down leases, putting money down on a used car lease reduces your capitalized cost, which further lowers your monthly payment. Be careful, though. Most financial experts advise against putting large down payments on leases. If someone totals the car in an accident a week later, the insurance pays the bank, and you lose your upfront money completely.

Helpful Tips for a Smooth Leasing Experience:

- Always check your credit report online before you visit the dealership. Fix any major errors that might drag your score down and cost you money.

- Call your insurance agent ahead of time. Give them the exact Vehicle Identification Number (VIN) of the used car you want to lease so you know exactly how much your premium will cost each month.

- Ask the dealer to explain the mileage limits clearly. Most used car leases allow you to drive 10,000 to 12,000 miles per year. If you commute long distances and drive more than that, negotiate a higher mileage limit upfront to avoid expensive penalty fees later.

Alternatives to Leasing a Used Car

If you discover that you cannot lease the specific used car you want, or if the dealer’s financial terms simply do not fit your monthly budget, you have several excellent alternatives to consider.

1. Financing a Used Car (Buying)

Instead of leasing, you can take out a traditional auto loan through a bank or credit union and buy the used car outright. When you finance a car, every single payment you make builds equity in the vehicle. Once you successfully pay off the loan, you own the car completely. You never have to worry about strict mileage limits or annoying wear-and-tear fees. While the monthly payment might be slightly higher than a used lease, purchasing almost always makes more financial sense in the long run. You can drive the car as far as you want, modify it, and sell it whenever you please.

2. Leasing a Cheaper New Car

If you desperately want the low payments of a lease but want to avoid the maintenance risks of an older vehicle, look at leasing a mainstream economy brand. Leasing a brand-new Honda Civic, Toyota Corolla, or Hyundai Elantra might cost the exact same amount per month as leasing a used luxury vehicle. You get the ultimate benefit of a full factory warranty, the newest safety technology, and zero miles on the engine.

3. Taking Over a Lease (Lease Transfer)

You can use specialized online websites to find drivers who want to get out of their current new car leases early. You can legally take over their lease contract. You essentially step into their shoes, make the remaining monthly payments, and return the car to the dealer when the term ends. This clever strategy allows you to drive a relatively new car with a very short commitment time and often requires absolutely zero down payment from your pocket.

To compare your top two used car choices, review this simple breakdown of leasing versus financing a used car:

| Feature | Leasing a Used Car | Financing a Used Car (Buying) |

|---|---|---|

| Ownership | You return the car to the dealer at the end of the term. | You own the car completely after you pay off the auto loan. |

| Monthly Cost | Lower, because you only pay for the car’s depreciation. | Higher, because you pay for the entire purchase price of the vehicle. |

| Mileage Limits | Strictly capped (usually 10,000 to 12,000 miles per year). | Unlimited. You can drive the car as much as you want. |

| End of Term | You can return it, buy it, or start a new lease. | You keep the car, sell it, or trade it in for a new vehicle. |

| Maintenance | You must maintain the car strictly to the dealer’s standards. | You control how and when you maintain the vehicle. |

Frequently Asked Questions

Can you negotiate a used car lease?

Yes, you absolutely can negotiate a used car lease. Just like a standard new car deal, you should aggressively negotiate the capitalized cost (the selling price of the car). You can also negotiate the mileage limit, the trade-in value of your current vehicle, and sometimes the money factor. You cannot, however, negotiate the residual value, as the lending bank securely sets that number and the dealer cannot change it.

Does Honda or Toyota allow you to lease a used car?

Yes, both Honda and Toyota offer highly rated used car leasing programs through their certified pre-owned departments. However, these programs usually run on a local or regional level, meaning not every single dealership chooses to participate. You must call your local Honda or Toyota franchise directly and ask the finance manager if they facilitate CPO leases.

Can I lease a 5-year-old car?

Generally, no. Most manufacturer-backed used car leasing programs strictly require the vehicle to be less than four model years old. Banks find it entirely too risky to predict the residual value of a five-year-old car, and older cars fall outside the safe boundaries of most certified pre-owned warranties.

Is car insurance more expensive for a leased used car?

No, car insurance for a leased used car typically costs less than insurance for a leased new car. Since auto insurance rates heavily depend on the total replacement cost of the vehicle, the depreciated value of a used car makes it noticeably cheaper to insure. However, remember that the leasing company will strictly require you to carry full comprehensive and collision coverage, which costs more than state-minimum basic liability.

What happens at the end of a used car lease?

When your used car lease reaches its official end date, you have three main options. First, you can return the car to the dealership, pay any disposition fees or mileage penalties, and walk away clean. Second, you can buy the car outright for the residual value stated clearly in your original contract. Third, you can hand the car over as a trade-in and start a brand-new lease on a completely different vehicle.

According to Experian, some dealerships offer leasing options for certified pre-owned vehicles, although it is less common than new car leasing.

Learn more about used car leasing