With gas prices constantly fluctuating and environmental awareness on the rise, millions of drivers are making the switch to hybrid vehicles. Hybrids offer a fantastic middle ground between traditional gas guzzlers and fully electric cars. However, when you finally pick out the perfect eco-friendly car, a major question pops up during the buying process: are hybrid cars more expensive to insure?

If you are budgeting for a new vehicle, you need to look past the sticker price and the fuel savings. Auto insurance is a major ongoing cost of car ownership. Many drivers feel surprised when they receive their first premium quote for a hybrid. They expect their eco-friendly choice to bring immediate savings across the board, but auto insurance calculates risk differently than the gas pump.

In this comprehensive guide, we will break down exactly how insurers view your hybrid vehicle. We will explore the mechanical and financial reasons behind premium differences, compare hybrid insurance vs gas insurance, and give you actionable tips to lower your monthly bill.

The Short Answer (TL;DR)

Yes, hybrid cars are generally 7% to 11% more expensive to insure than their standard gas-powered counterparts. Insurance companies charge higher premiums for hybrids primarily because they have a higher initial purchase price and contain complex, specialized parts—like heavy-duty battery packs—that cost more to repair or replace after an accident.

Why Are Hybrid Cars More Expensive to Insure?

To understand why your insurance bill looks a little higher, you have to think like an insurance adjuster. Auto insurance companies do not base premiums on how much fuel you save. They base premiums on risk and payout costs. If you get into an accident, how much money will the insurance company have to spend to fix your car or replace it entirely?

For hybrid vehicles, that repair and replacement cost is simply higher than it is for traditional internal combustion engine (ICE) vehicles. Let’s break down the three main reasons why hybrids are expensive to insure.

1. Higher Initial Purchase Price (MSRP)

Hybrids cost more money straight off the dealership lot. Building a car that contains two different power sources (a gas engine and an electric motor) requires more materials and advanced engineering. Because the Manufacturer’s Suggested Retail Price (MSRP) is higher, the car holds a higher overall value.

If your hybrid gets totaled in a severe accident, your collision and comprehensive coverage must pay out the actual cash value of the vehicle. Since the vehicle is worth more money, the insurance company takes on a larger financial risk. They offset this larger risk by charging you a higher monthly premium.

2. Specialized Parts and Hybrid Batteries

Under the hood, a traditional gas car is a known entity. Mechanics have repaired them for over a century. A hybrid car, however, is a highly complex machine. It utilizes a dual-engine system. You have the standard combustion engine parts, plus complex wiring, electric motors, regenerative braking systems, and most importantly, the high-voltage battery.

These batteries—usually made of lithium-ion or nickel-metal hydride—are incredibly expensive. If a minor fender bender damages the hybrid battery pack, a repair bill that might have cost $1,000 on a standard car can suddenly skyrocket to $4,000 or $5,000. Insurers know that one damaged battery means a massive claim payout.

3. The Need for Specialized Mechanics

You cannot take a damaged hybrid to just any local body shop. Working on high-voltage electrical systems requires specialized training, unique tools, and strict safety protocols to prevent electrocution.

Because these technicians possess specialized skills, their hourly labor rates are noticeably higher than standard mechanic rates. When an insurance company cuts a check for collision repairs, they must cover this higher labor cost. Ultimately, those higher repair costs trickle down to the consumer in the form of higher insurance premiums.

The Cost Breakdown: Hybrid vs. Gas Insurance

How much more does it actually cost to insure a hybrid vs a gas car? While individual rates vary wildly based on your age, driving record, and location, looking at national averages helps paint a clear picture.

According to industry data from automotive researchers like Kelley Blue Book and various insurance aggregates, drivers usually pay around $100 to $200 more per year for hybrid auto insurance compared to identical gas models.

Let’s look at a realistic hypothetical comparison based on national averages for a standard sedan versus its hybrid variant.

| Vehicle Type | Average Annual Premium | Monthly Cost Breakdown | Estimated Fuel Savings (Yearly) |

|---|---|---|---|

| Standard Gas Vehicle (e.g., Honda Accord) | $1,550 | $129 / month | $0 (Baseline) |

| Hybrid Vehicle (e.g., Honda Accord Hybrid) | $1,700 | $141 / month | Saves approx. $400 – $600 |

| The Difference | +$150 / year | +$12 / month | Net Positive Savings |

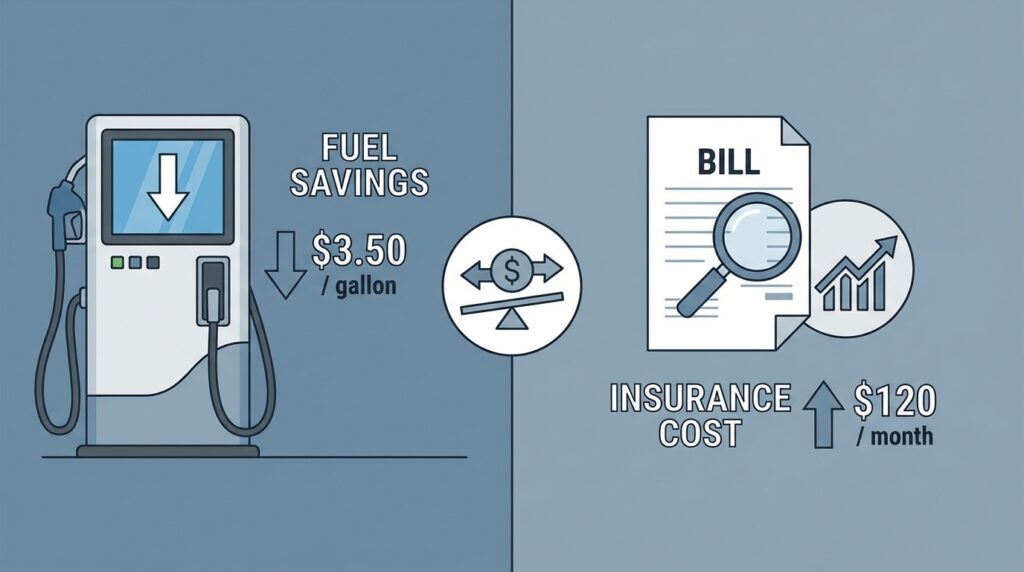

As the table highlights, you might pay an extra $150 a year for insurance. However, the hybrid vehicle will likely save you $500 a year at the gas pump. When you calculate your total cost of ownership, the hybrid almost always wins. The fuel savings easily swallow the slight bump in insurance costs.

Hybrids vs. EVs: Which Costs More to Insure?

When shopping for a green vehicle, you might feel torn between a hybrid and a fully electric vehicle (EV) like a Tesla or Ford Mustang Mach-E. If insurance costs concern you, you need to understand how the insurance industry categorizes these different technologies.

- Standard Hybrids (HEVs): These cars charge their own batteries using regenerative braking and the gas engine. You never plug them in. Insurance is moderately higher than gas cars.

- Plug-in Hybrids (PHEVs): These feature larger batteries that you plug into a wall outlet, offering 20 to 40 miles of pure electric driving before the gas kicks in. Insurance is slightly higher than standard hybrids due to the larger battery pack.

- Electric Vehicles (EVs): These cars rely 100% on massive battery packs. They have no gas engine at all. EVs are currently the most expensive to insure out of the three.

“Electric vehicles carry the highest insurance premiums in the green car sector. Their massive battery packs often make up a huge percentage of the car’s total value. If an EV battery is structurally compromised in a crash, insurers frequently total the entire vehicle.”

If you want to reduce your carbon footprint without taking on the highest possible insurance rates, a standard hybrid or a plug-in hybrid serves as the perfect financial middle ground. You get excellent gas mileage without the extreme repair risks associated with fully electric vehicles.

How to Lower Your Hybrid Car Insurance Rates

Just because insurers charge a premium for hybrid vehicles does not mean you are stuck paying top dollar. Smart shoppers can take several practical steps to drive their premiums down. Here is how you can get cheaper insurance for your hybrid.

1. Ask for “Green Vehicle” Discounts

Many major insurance providers want to attract environmentally conscious drivers. Actuarial data often shows that people who buy hybrids tend to drive more cautiously and get into fewer reckless accidents. Because of this, companies like Travelers, Farmers, and Liberty Mutual offer specific “Alternative Energy” or “Green Vehicle” discounts. You can often save between 5% and 10% just by asking your agent to apply this discount to your policy.

2. Shop Around and Compare Quotes

Never accept the first insurance quote you receive. Every auto insurance company uses a different secret formula to calculate risk. One company might penalize hybrid owners heavily, while another company might barely charge an extra fee. Whenever you buy a new car, you should get quotes from at least three to five different providers to find the most competitive rate.

3. Bundle Your Policies

Bundling remains one of the easiest ways to save money on insurance. If you currently rent an apartment or own a home, make sure you buy your auto insurance from the same company that provides your renters or homeowners insurance. Insurers love loyal customers, and bundling can strip 10% to 20% off your total bill, completely erasing the hybrid penalty.

4. Increase Your Deductible

Your deductible is the amount of money you agree to pay out of pocket before your insurance coverage kicks in. If you have a $500 deductible, consider raising it to $1,000. By taking on a little more financial responsibility in the event of a minor scrape, the insurance company will reward you with a noticeably lower monthly premium. Just ensure you keep that $1,000 safe in an emergency savings account.

5. Maintain a Clean Driving Record

At the end of the day, your driving habits matter far more than the type of engine in your car. Speeding tickets, at-fault accidents, and DUI convictions will skyrocket your premiums regardless of what you drive. Drive safely, follow the speed limit, and avoid distractions. A clean driving record guarantees you the lowest possible base rate.

Frequently Asked Questions

Is insurance for a Toyota Prius expensive?

The Toyota Prius is the most famous hybrid in the world. Because there are millions of them on the road, parts are actually much easier to find than parts for rare luxury hybrids. While a Prius does cost slightly more to insure than a standard compact gas car (like a Toyota Corolla), it remains one of the cheapest hybrid vehicles to insure on the market today. Its excellent safety ratings help keep premiums reasonable.

Does hybrid auto insurance cover battery replacement?

This depends entirely on how the battery breaks. If you get into a car accident and the collision damages the hybrid battery, your collision insurance will absolutely cover the cost of a replacement battery (minus your deductible). However, if your battery simply dies from old age and natural wear-and-tear after 100,000 miles, standard auto insurance will not cover it. Insurance covers sudden accidents, not mechanical maintenance.

Do hybrids get stolen more often?

Generally, no. However, hybrids are prime targets for a specific type of theft: catalytic converter theft. Hybrids have high-quality catalytic converters that contain larger amounts of precious metals (like rhodium and palladium) because the gas engine doesn’t run constantly to keep them hot. Comprehensive insurance covers catalytic converter theft, which is another minor reason insurers charge slightly more for hybrid coverage.

Conclusion

So, let’s recap: are hybrid cars more expensive to insure? Yes, you can expect to pay around 7% to 11% more for your auto insurance policy. The combination of a higher MSRP, expensive battery technology, and specialized repair mechanics forces insurance companies to charge slightly higher premiums to cover their risks.

However, you should never let this discourage you from buying a hybrid. The incredible fuel savings, the smooth driving experience, and the positive environmental impact far outweigh the extra $10 to $15 a month you might spend on auto insurance. By shopping around, utilizing green discounts, and keeping a clean driving record, you can easily manage the costs.